The Suited Investment Banking Study Guide

.png)

The Suited Investment Banking Study Guide

If you want to secure an internship at an investment bank this or any summer, there are certain “technical skills” that are crucial to understand. In this study guide, you will find a basic summary of what most firms will expect you to know in your interviews.

This study guide is meant to give those who may not have access to certain resources a proper starting point and overview on how all of the necessary financial concepts flow together. There certainly exist more comprehensive guides that will walk you through specific questions and how to answer them, but our goal is to drive an understanding of these technical concepts as a whole.

Before diving in, we recommend you check to see if your school’s career center has access to Vault or other IB prep guides. Look for and download their guides to Investment Banking and Investment Banking Interviews. These resources will teach you most of what you need to know for the interview, and everything else can be learned on the job. Additionally, there are lots of free resources online that provide a more in-depth look at these concepts. We like the free definitions provided by Investopedia and the free concept descriptions and sample models provided by Macabacus.

The three areas of finance you should be familiar with before an interview are:

- Basic Accounting | Know how to read an Income Statement, a Balance Sheet, a Cash Flow Statement, and how they all intersect.

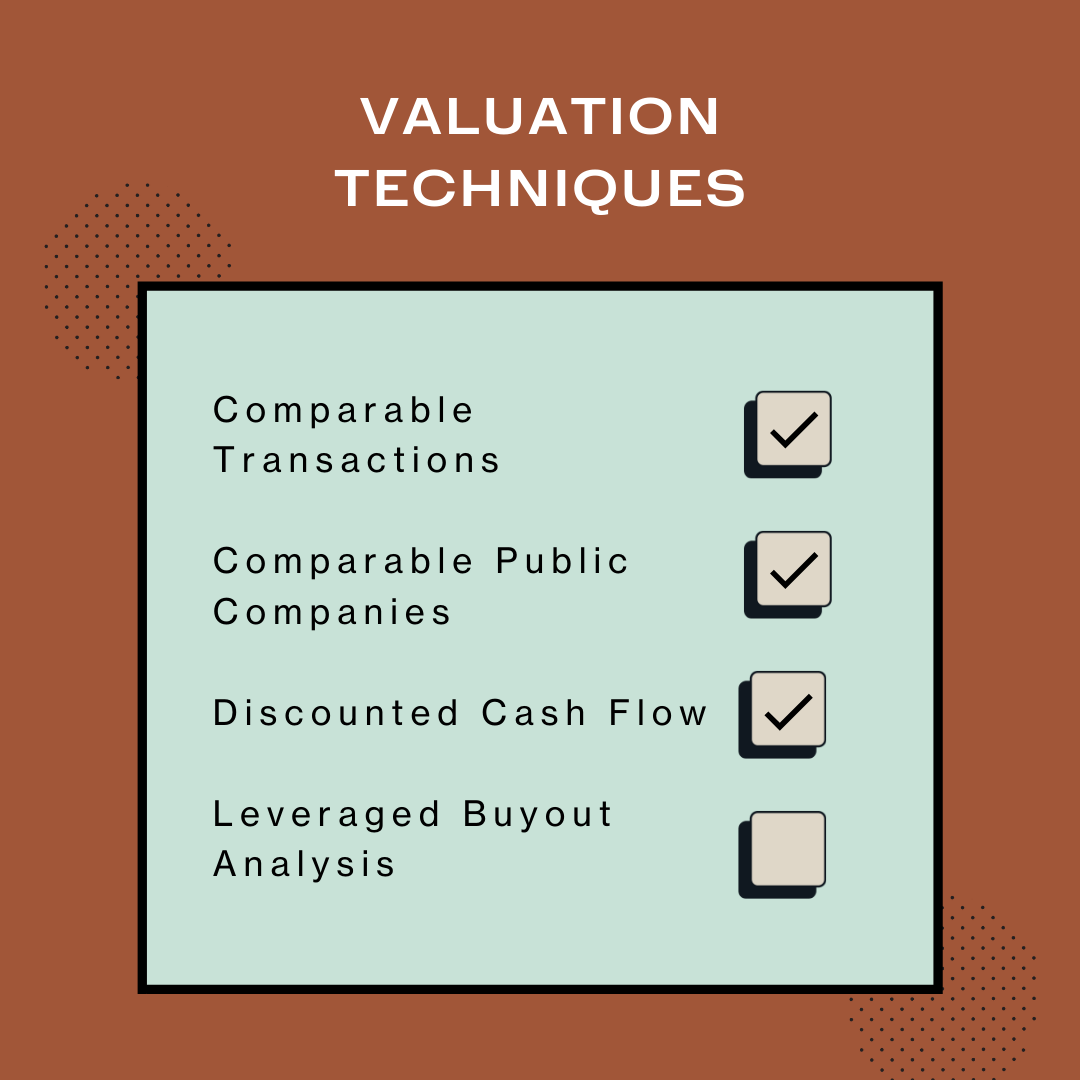

- Valuation Methods | Understand the four main valuation techniques (Comparable Transactions, Comparable Public Companies, Discounted Cash Flow, Leveraged Buyout) and how assumption changes in each impact implied value.

- Transaction Process | Learn how major financial transactions get executed.

01.

Basic Accounting

Accounting is the foundation of investment banking because a thorough understanding of how companies measure and report their financial health is fundamental to all valuation and deal-making. Luckily, for those who haven’t taken Accounting or for those who hated the class, the accounting you need for investment banking is simple. You don’t need to understand financial reporting and audit concepts, like debits and credits, general ledgers, or trial balances. Investment Bankers just need to understand how to read financial statements and what they mean in practice as it relates to a business’s health. Specifically, bankers are most concerned with how much cash a business generates and can expect to generate in the future.

In particular, you should get comfortable with the three financial statements: the Income Statement (“IS”), the Balance Sheet (“BS”), and the Cash Flow Statement (“CF”).

You should understand the following things about each one of these statements.

The Income Statement: The IS reflects the performance of the business based on accrual accounting rules and includes both cash and non-cash revenue and expenses.

The Balance Sheet: The BS represents a snapshot of the business’s assets and liabilities, starting with cash balance (from a prior period plus cashflow from the CF statement).

The Cash Flow Statement: The CF bridges the Income Statement’s final line, Net Income, to actual cash flow by adding back non-cash expenses, like depreciation. The CF also reflects cash expenses not captured on the IS, like capitalized investments in equipment and purchases of inventory, as well as adds in (or subtracts) cash flow from financing activities, such as proceeds from selling equity.

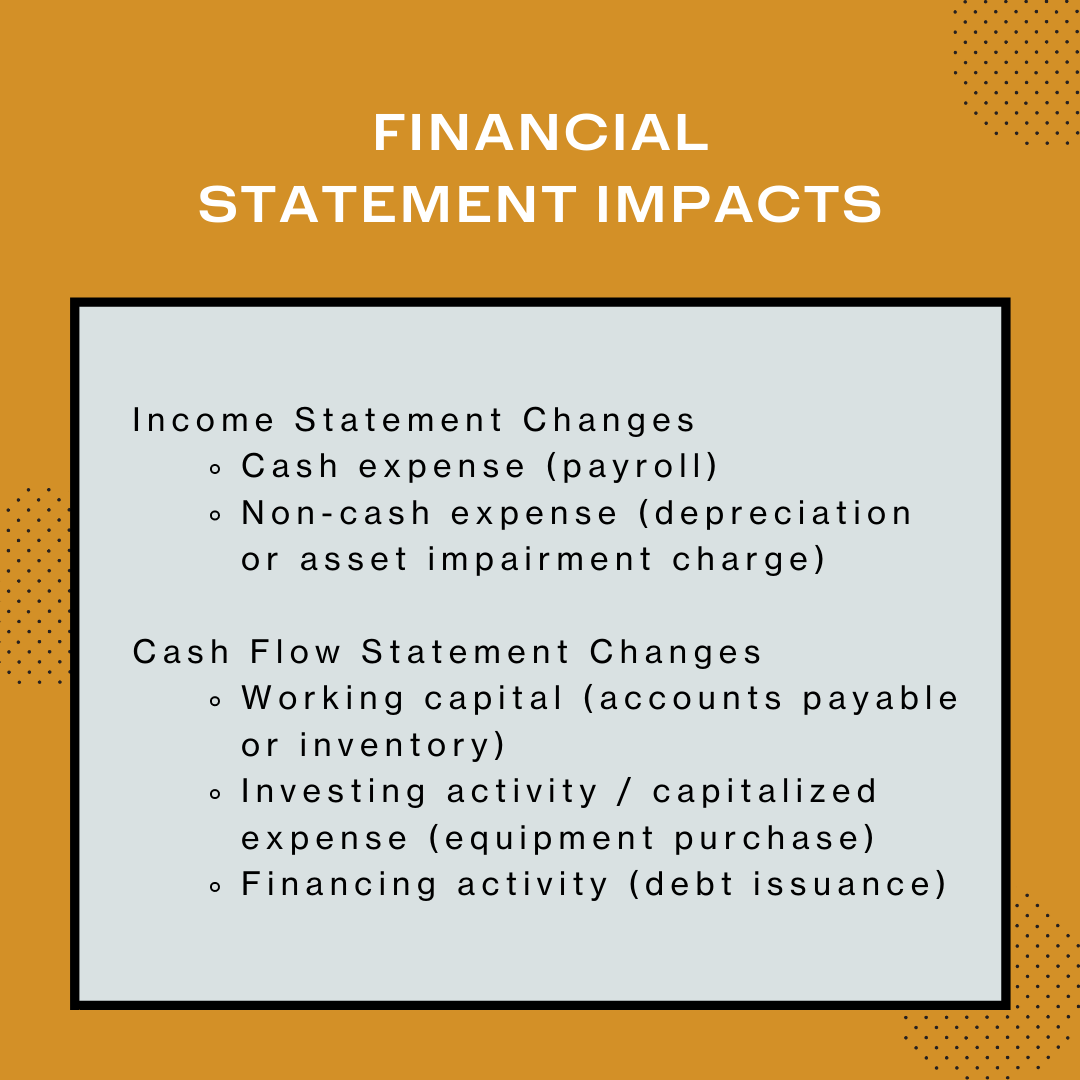

Typically, interviewers evaluate accounting concepts by asking you to describe how a change in one item on a financial statement would flow through to the other two statements. This competency check may take the form of a question like:

Walk me through the purchase of a $10 piece of equipment that is capitalized and how it impacts all three financial statements at year 0 and year 1.

You’d need more information to answer that question, such as the depreciable life (let's say, 5 years) and the tax rate (let's say, 20%), and sometimes interviewers will expect you to ask for the information needed that isn’t provided.

The short answer: if a purchase is capitalized, there is no change to the IS in year 0 - the purchase shows up on the CF (cash flow from investing down $10) and on the BS (cash balance down $10 and assets up $10).

Then, in year 1, a non-cash depreciation charge of $2 (assuming straight-line depreciation, $10 equipment / 5 year life = $2 annual depreciation) hits the IS, which reduces earnings before tax by $2. This reduces the tax liability, so the impact to net income is $2 x (1-20%) = net income down $1.60. Net income flows through to the top of the CF where the non-cash depreciation charge of $2 is added back, increasing cash flow by $0.40 (the tax savings). On the balance sheet, cash is up $0.40, assets are down $2 (the depreciation with the equipment now shown as $8 in value) for a net change in assets of -$1.60. And net income from the IS of -$1.60 flows from the income statement into retained earnings (a component of equity on the BS), allowing the BS to balance!

There are lots of ways to ask this type of accounting question (by referencing any of the line items on a financial statement), but once you have a thorough understanding of how each line item is calculated and relates to each other, you will ace these questions.

In particular, you should focus on how an increase or decrease in any of the following will impact each of the financial statements and ultimately how they impact and result in a balanced balance sheet (where assets = liability + shareholders equity):

You’ll also want to know how to calculate EBIT (Earnings Before Interest and Tax) and EBITDA (EBIT + Depreciation and Amortization). These non-GAAP metrics are commonly used by investment bankers to evaluate the earnings and cash a business generates without consideration of how much debt a business has.

These earnings metrics are, therefore, more comparable between businesses than things like Net Income, which are influenced by how much debt (and therefore interest) a company has.

02.

Valuation

Once you have an understanding of basic accounting, you’ll want to develop confidence with valuation concepts so you can use the historical and forecast IS, BS, and CF to determine what the business is worth. In particular, you should focus on: Comparable Transactions, Comparable Public Companies, Discounted Cash Flow analysis (“DCF”), and Leveraged Buyout analysis (“LBO”).

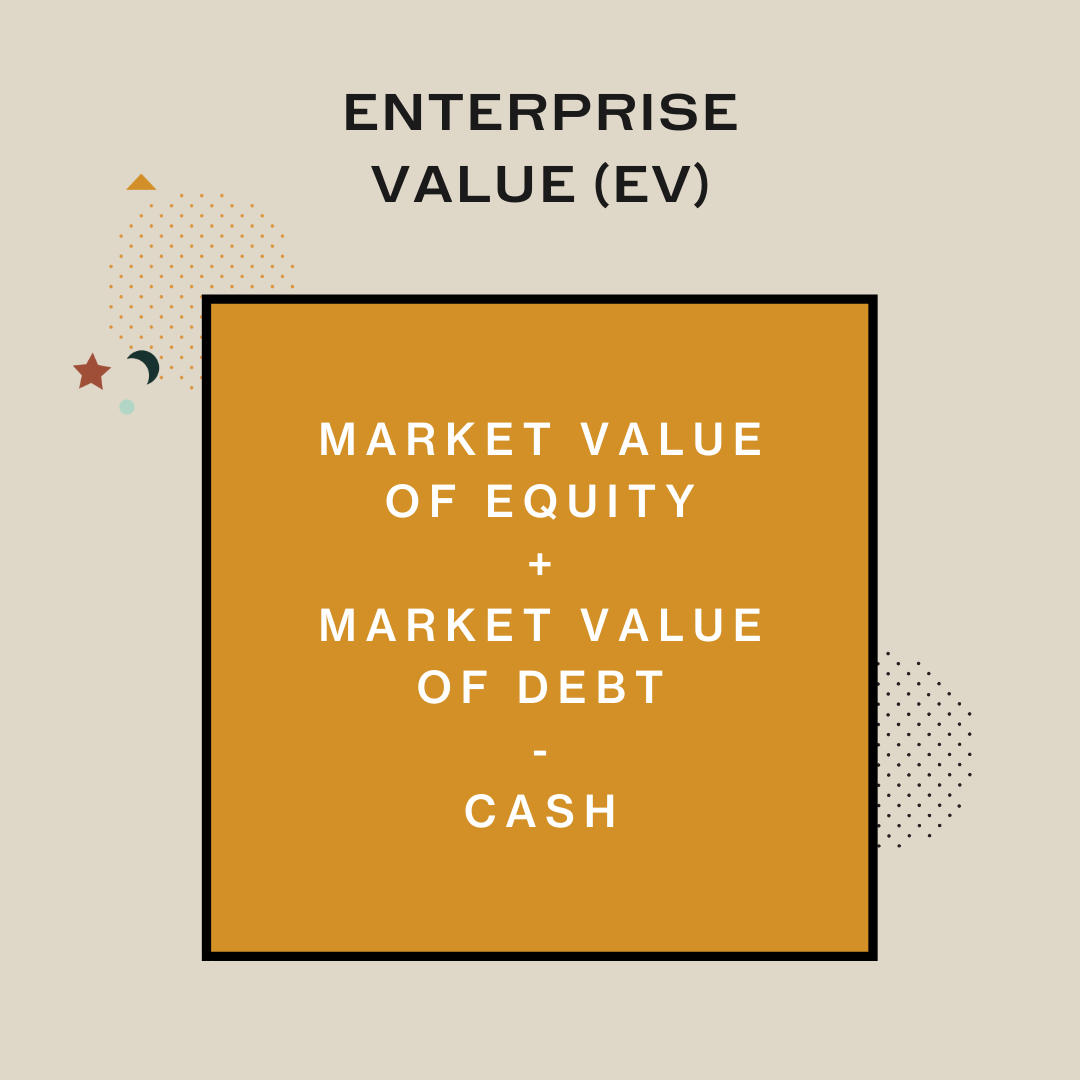

But before jumping into any valuation technique, it’s important to understand how to calculate the main metric of business value: Enterprise Value (“EV”). EV is the value of the operations of a business and represents the value of all equity ownership and debt claims on the business:

Why exclude cash? Because cash isn’t an operating asset; cash is cash whether it’s on Google’s or Ford’s balance sheet (two very different businesses). It doesn’t speak to the value of the business operations; EV allows us to compare businesses value, not cash value. Valuation techniques are mostly about estimating EV. Then if you want to calculate equity value, you can just add in cash and subtract debt. It’s that easy!

Back to the valuation techniques:

COMPARABLE TRANSACTIONS

If you want to understand what a house is worth, it would be a great idea to figure out what similar houses in similar areas have sold for before. But houses come in all shapes and sizes, so you would have to adjust each to calculate a price / square foot. You could also calculate price / bedroom, or price / window, really any way you

think appropriate to equalize the comparison.

That’s the same idea with comparable transaction analysis. It involves finding similar businesses that have sold recently and calculating how they were valued (EV) as a ratio to what the business earned at the time of the transaction. Common ratio are EV / Revenue, EV / EBIT, and EV / EBITDA. Once you find the most relevant transactions, you can calculate an average valuation ratio and then multiply it by the same earnings metric for the business you’re evaluating to estimate its EV.

Typically, all you need to have for interviews is a basic understanding of how the analysis works. You might hear a question like, "What would you do if a business has negative EBITDA?” Just consider EV / Revenue (or a DCF and LBO).

COMPARABLE PUBLIC TRANSACTIONS

Comparable public companies are similar, but instead of looking at previous transactions, you would calculate the average valuation ratio of similar publicly traded companies. This involves first looking at a company’s Stock Price x Shares Outstanding to calculate Equity Value (market capitalization). Then you would add in debt and subtract out cash to calculate EV. Just as with comparable transactions, you would calculate a valuation ratio for each company and then use the average ratio to value the business you're analyzing.

DISCOUNTED CASH FLOW ("DCF")

While the first two analyses compare a business to other businesses, a DCF is a valuation technique that looks at how much cash a business expects to generate. Interviewers might ask you to “walk me through a DCF," which just means to describe the major lines and calculations you would use to get to a valuation.

Put simply, a DCF looks at how much cash a business expects to generate for all investors, and then values the cash flows based on the likelihood (or risk) that the business achieves that forecast relative to other potential investments. Said differently, a DCF values the cash flows based on the return the investors would require to be willing to invest in the business relative to other opportunities available to them.

There are two main calculations in a DCF: the value of cash the business generates every year during the period forecast and the value of the business in perpetuity after the forecasted period.

Value of the Cash The Business Generates

The main cashflow metric in a DCF is called “unlevered free cash flow” and can be thought of as the cash a business generates before it pays anything to the investors - before interest is paid to creditors and before dividends are paid to shareholders. It is calculated as follows:

To value the cash flow a business expects to generate, you would first calculate the business’s unlevered free cash flow for each forecast period (typically 5-10 years). You then “discount” the cashflows to a present value based on the return required by investors. This is accomplished using a simple formula:

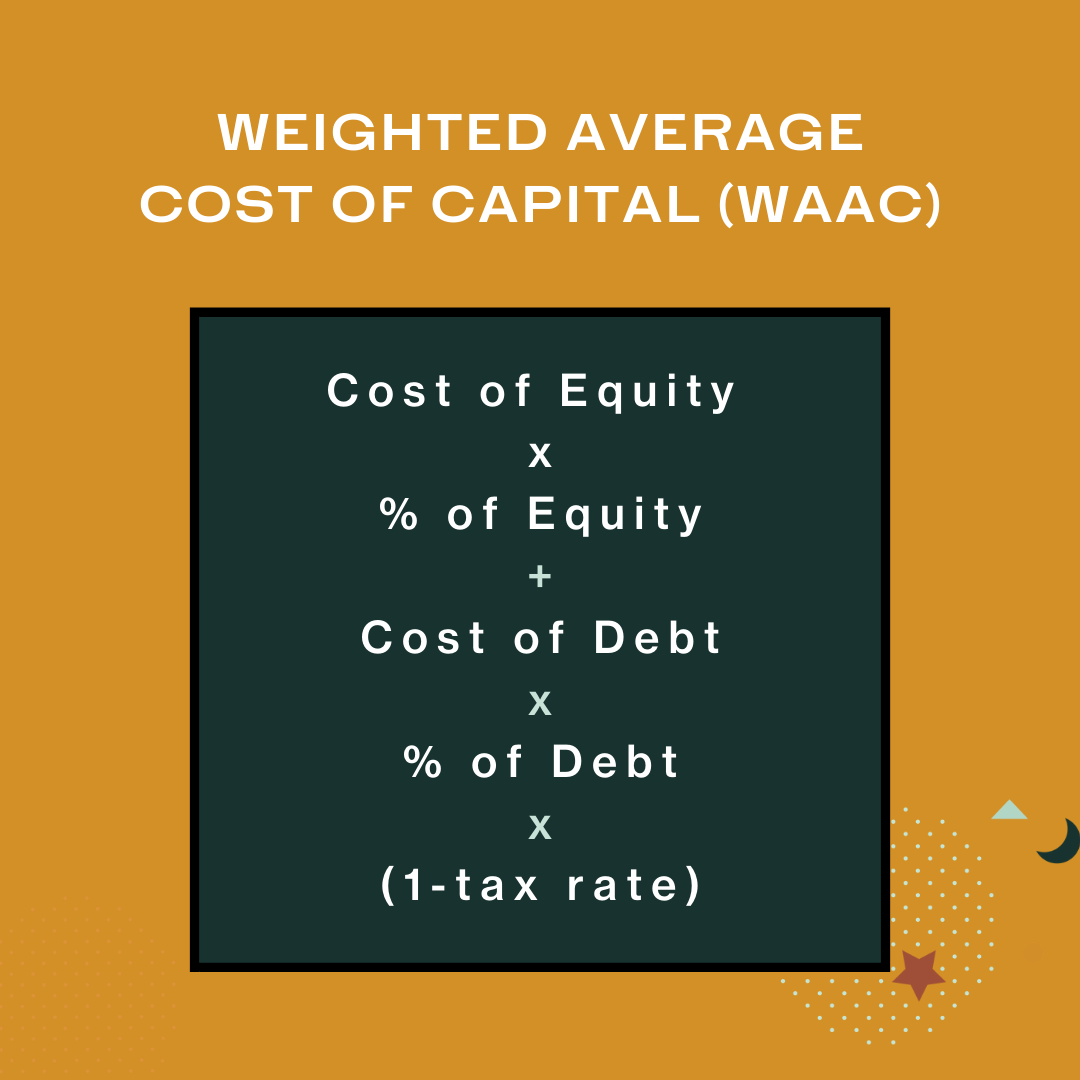

The Discount Rate in a DCF is the Weighted Average Cost of Capital, or “WACC”, which represents the blended return required by a debt and equity investor. It’s calculated as follows:

Each of the inputs to the WACC calculation are typically based on similar businesses' cost of equity and cost of debt, as well as their average split of debt and equity.

While the cost of debt is simple (the interest rate), the cost of equity is a complicated formula based on something called “CAPM”. It is unlikely interviewers will ask you anything about CAPM, but feel free to look into it if you’re feeling fancy. Once you have calculated Unlevered Free Cash Flow and WACC, you can easily discount each cash flow to a “present” value. Add all of them up to get the present value of the forecasted cash flows.

Value of the BUSINESS IN PERPETUITY

The final piece of the DCF is the value of the business in perpetuity after the forecast, also known as the “terminal value.” This is typically accomplished by either assuming the business is sold / acquired (by calculating a sale value, such as by assuming an EV / EBITDA sale multiple), or by using something called the Gordon Growth Method. We won’t go into the details of the Gordon Growth Method here but you should make sure you’re generally familiar with it. It’s complicated theory but simple math.

Once you’ve calculated the terminal value, you’d just discount it back to a present value based on the period (e.g. at the end of the forecast, such as 5 or 10 years from now) and the discount rate, just as with the forecast cash flow.

To calculate the final DCF value, you’d just add up the present value of the forecast cash flow and the present value of the terminal value. It sounds a bit complicated, but it won’t feel that way once you get the hang of it.

Of course, a lot of the DCF method is based on assumptions: assumptions around the business forecast, assumptions of the returns required by investors, and assumption around the potential long-term growth or acquisition value of a business. Investment bankers will analyze value implied by a DCF by changing, or “sensitizing,” these major model inputs in order to determine potential valuation ranges - they might show what the value would be at different revenue growth rates, or at different discount rates.

What questions should you be prepared for as it relates to DCF? In addition to being asked to "walk through a DCF," we expect you may hear something like this:

Explain if the value of a business will increase or decrease if you change [INSERT] assumption.

This type of question demonstrates you have a working knowledge of how all the pieces of a DCF fit together. For example, an interviewer might ask how the value of a business changes if accounts receivable go up. Accounts receivable are an element of working capital representing customers who owe you money but haven’t paid yet. If that balance goes up, the amount of cash you're owed goes up, so the cash you actually receive goes down. If cash flow decreases, the value of the business based on a DCF goes down. This type of question is common because it relies on accounting skills to understand impact to cash flow and valuation knowledge to know how it will impact the result. So you have to master your basic accounting skills too!

LEVERAGED BUYOUT ANALYSIS ("LBO")

Questions about LBOs are a little less common in summer internship interviews. But while it’s a more complex valuation technique, once you understand the DCF, it will be easy to understand how an LBO works just in case it comes up.

We won’t go into too much detail here, but we think the easiest way to understand an LBO is to think about it just like a DCF but from just the perspective of an equity investor (rather than debt and equity investors together). Putting your equity investor hat on, an LBO analysis asks the question “if I can expect to sell this business in a few years at X price, what can I pay for it today in order to generate the return I’m looking for, say, 25%”. To increase returns, as an equity investor I can finance some of the purchase price with debt, reducing how much I have to invest to purchase the business. And if the business performs well and grows, the cash flows may be used to pay off the debt and, if I can sell it for more than I purchased it for, allow me to realize a higher return as a percentage of my initial investment.

All of this requires assumptions of the business forecast, the debt available to finance the purchase, the interest and debt payback terms, the sale value at the end of owning the business, and the return required by the investor.

There’s a lot of detail here, but we’d recommend focusing on how changing these main assumptions impact the value implied by an LBO analysis. If you understand the general framework, they are fairly straight-forward questions. For example, increasing the debt available to finance the purchase, all else equal, would increase the value of the business because the equity investor can borrow more and therefore pay more while maintaining their investment amount. Alternatively, all else equal, if the investor has a higher return requirement, they are not able to invest as much at the beginning to realize the expected sale proceeds, so the implied value of the business would be lower.

03.

Transaction Process

The final area of technical questions may relate to how transactions are typically completed. This includes all of the logistics, timelines, and legal requirements of selling or buying a business, raising debt or equity capital, or restructuring a company. Each transaction type is unique and is worth learning about at a high level. You should focus on the transaction types where you are interested in pursuing a career as most investment banks separate by specialization area. When you interview, you will most likely interview with a person who specializes in one of these areas, and you should be prepared to answer related questions.

Want to stay in the loop?

Subscribe to our e-mail list for Suited-related updates, or visit our Newsroom here.